Why ITM Covered Calls Beat OTM

Algolearn.AI February 27, 2026 6 min read 637 views

The default covered call strategy most traders learn first is to sell out-of-the-money (OTM) calls: collect premium, keep your shares, and hope the stock isn't called away. It's clean, intuitive, and feels safe. But it isn't the only approach, and for income-focused positions it often isn't the best one.

This article makes the case for selling in-the-money (ITM) covered calls — how they work, why they generate more reliable income, and why early assignment is unlikely.

Time Value Is the Whole Game

A common misconception about ITM calls is that because the option is in the money, all of its value is intrinsic — that the buyer is only paying for the gap between the strike price and the current stock price, leaving nothing for the seller.

That's incorrect. An ITM call at 30 days to expiration (DTE) still carries meaningful extrinsic value — time value — in its premium. The market is pricing in thirty days of possibility: the stock could move further, volatility could spike, conditions could change. That uncertainty has a price, and a buyer is willing to pay it.

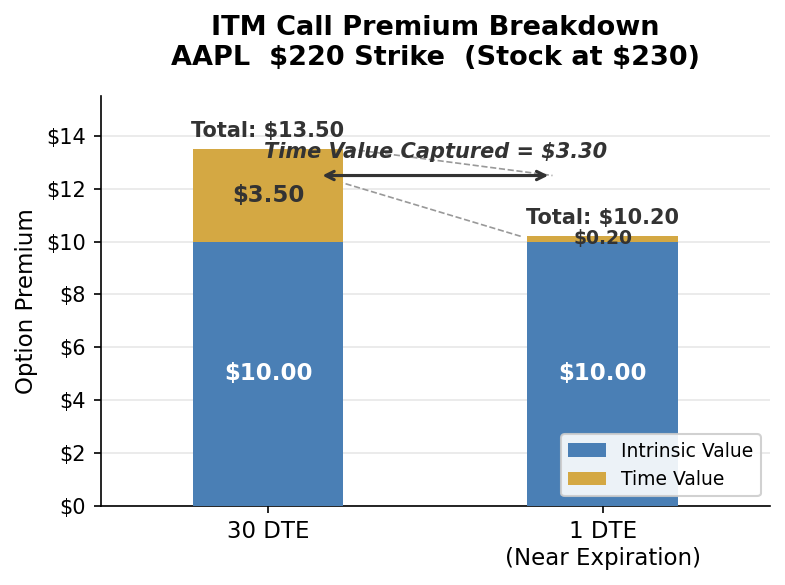

A concrete example. Suppose you own 100 shares of AAPL at $230 and sell a 30 DTE call with a $220 strike — $10 in the money. The option might be priced at $13.50. Ten dollars of that is intrinsic value (the $230–$220 gap). The remaining $3.50 is time value — and that time value is the entire point of the strategy.

This chart shows how an ITM call's premium breaks down at 30 DTE versus near expiration. The intrinsic value — that $10 gap between stock price and strike — stays roughly constant. But the time value shrinks as expiration approaches. At 30 DTE, there's still $3.50 of extrinsic value sitting on top. By expiration, it's nearly zero. The shaded area between those two time-value levels is the profit zone — that's what you're harvesting.

The Roll

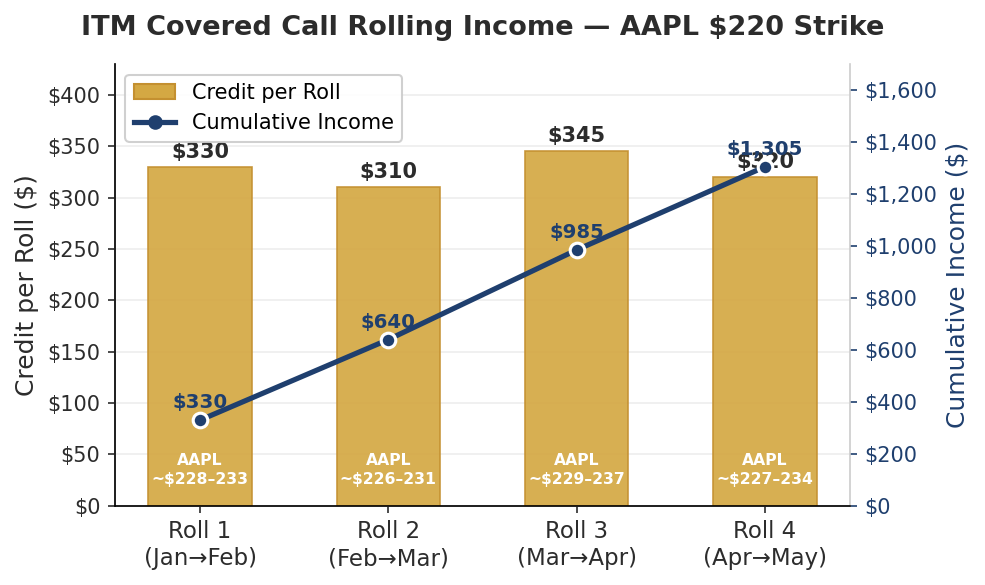

The mechanics of rolling an ITM covered call are straightforward. As your 30 DTE ITM call approaches expiration with the stock still at $230, your $220 strike call is now worth about $10.20 — almost entirely intrinsic value, with roughly twenty cents of time value remaining.

You buy that call back for $10.20, then sell a new $220 strike call — same strike, fresh 30 days on the clock. The new call is priced around $13.50 again: the same $10 of intrinsic value, plus a fresh $3.50 of time value as the market prices in another month of uncertainty.

The math:

- Buy back expiring call: -$10.20 (intrinsic + $0.20 time value)

- Sell new 30 DTE call: +$13.50 (intrinsic + $3.50 time value)

- Net credit: $3.30 per share, or $330 per contract

That $330 of time value is captured without changing your strike, giving up your shares, or taking on new directional risk. The intrinsic values cancel out — you pay $10 of intrinsic on the buy-back and collect $10 of intrinsic on the new sell. The profit comes entirely from the difference in time value: you buy back an option with almost no time value left and sell one with thirty fresh days of it. Then you repeat the cycle every thirty days.

This chart tracks four consecutive rolling cycles on AAPL at the $220 strike over roughly four months. Each cycle shows the buy-back cost, the new sell credit, and the net credit captured. Cycle 1: net credit $330. Cycle 2: $310. Cycle 3: $345. Cycle 4: $320. The cumulative income line climbs to $1,305 over the period. Stock price fluctuates between $226 and $237 throughout — the strike stays ITM the whole time, and the rolls keep producing income regardless of whether the stock drifted up or down within that range.

Why Early Assignment Is Unlikely

The most common concern with ITM covered calls is early assignment. In practice, it rarely happens, and the reason is rooted in the option's economics.

Consider the buyer's position. They hold an ITM call with, say, 15 days left, worth $12 — $10 of intrinsic value and $2 of time value. Exercising the option gets them shares at the strike and captures the $10 of intrinsic value, but it destroys the remaining $2 of time value. Selling the option on the open market for $12 instead captures both the intrinsic and the time value. Exercise is almost always economically inferior to selling, because exercising forfeits whatever time value remains.

The main exception is dividends: if a stock is about to go ex-dividend and the dividend exceeds the remaining time value, early assignment becomes rational. Outside that narrow window, the time value in an ITM call functions as a shield against early assignment — as long as meaningful time value remains, the shares are unlikely to be called. The time value is simultaneously the product (your income) and the insurance (your assignment protection).

ITM vs. OTM Covered Calls

OTM covered calls are a legitimate strategy, but they involve different trade-offs:

OTM calls offer less premium and more directional risk. The credit is smaller because there's no intrinsic value — you're selling pure time value and hoping the stock doesn't push past your strike. If it does, your upside is capped and your shares are called away at a price that looks cheap relative to where the stock moved.

ITM calls offer more premium and a built-in cushion. Selling a call below the current stock price provides downside protection equal to the time value collected. If AAPL falls from $230 to $227, the position is still fine — the $3.50 of time value collected lowers the effective break-even, and the declining intrinsic value works in your favor on the buy-back.

The trade-off: ITM calls cap upside at the strike from the start. If AAPL runs to $250, that move isn't captured; the shares are called at $220, offset by the income collected along the way. This is why ITM covered calls suit positions held for consistent income rather than stocks expected to make large directional moves — a different goal calls for a different tool.

The Expected-Value Case

ITM covered calls are unglamorous by design. The returns are steady and the P&L curve resembles a slow staircase rather than a rollercoaster. There are no outsized plays to point to — just a small, reliable credit captured on each roll.

The strategy is an expected-value play. Expected value isn't about any single outcome; it's about what the process produces over many repetitions. Each roll captures a modest, dependable credit, and over dozens of cycles those credits compound into meaningful income. The edge is in the math, executed with discipline, repeated consistently.

Risks and Limitations

A few honest caveats apply:

- Theta decay isn't always smooth, and the pace of time-value erosion can vary across the cycle.

- Implied volatility can compress or inflate time value in ways that make the rolls less predictable.

- Dividends are a genuine assignment risk — ex-dividend dates need to be monitored closely.

- Market regime matters. The strategy performs best in sideways-to-slightly-bullish conditions; a sustained crash will test it, and capped upside means it underperforms in strong rallies.

Used on long-term positions in the right conditions, ITM covered calls trade flashy upside for steady, repeatable income — quiet money, collected month after month, while the rest of the market argues about direction.